- Startup Intros

- Posts

- Weekly Download #46

Weekly Download #46

Apple's CEO Cook Steps Down + OpenAI's $852B Identity Crisis + The AI Coding Gold Rush

Dev Chandra

April 20, 2026 • Estimated Reading Time: 8 minutes

Sponsored by

Hi !

This week in Silicon Valley, startups & tech:

Tim Cook is stepping down as Apple CEO after 15 years. John Ternus, the hardware chief who built Apple Silicon and Vision Pro, takes over Sept 1.

Amazon is investing another $25B into Anthropic on top of $8B already committed. Anthropic will spend $100B+ on AWS infra over 10 years.

OpenAI's $852B valuation is under scrutiny from investors. A leaked CRO memo reveals "Spud" model & claims Anthropic inflates revenue by $8B.

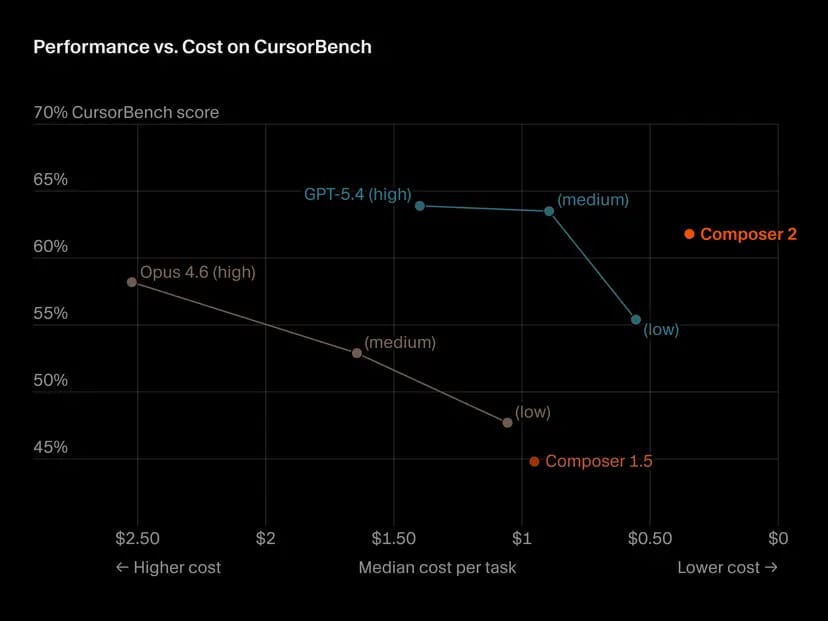

Cursor is raising $2B at a $50B+ valuation. GitHub Copilot paused new signups after costs doubled. Google formed a coding agent strike team.

Global DRAM supply will meet only 60% of demand through 2027. Mac wait times hit 12 weeks. Meta raised Quest 3 prices $100.

Startup Intros has a simple mission: to help early-stage founders stay informed and navigate fundraising from compliance to capital.

🔥 Startup Intros Events Coming Up

Apr 28-29: Startup Grind Conference: 5,000+ founders, investors & operators at the Fox Theatre in Redwood City, and we're planning a happy hour! Get $100 off with code STARTUPINTROSGC!

🍎 Apple's Changing of the Guard

👤 The Cook Legacy

Grew from a $350B market cap to over $4T (1,000%+ increase)

Revenue nearly quadrupled from $108B to over $416B

Launched Apple Watch, AirPods, and Vision Pro

Turned Services into a $100B+ annual business

After 15 years, Cook is stepping down and becoming executive chairman, where he will focus on global policy engagement as Apple navigates tariff pressures, EU regulation, and semiconductor supply chain disruptions.

🔧 The Ternus Bet

Joined in 2001 and spent 25 years rising through hardware engineering

Oversaw Apple Silicon, the custom chip architecture moving away from Intel

Shepherded Vision Pro from concept to launch

Johny Srouji moves into a newly created Chief Hardware Officer role, adding hardware engineering to his chip design responsibilities. AAPL dipped in after-hours trading. Analysts see it as a signal Apple will seek differentiation through physical products even as it reframes every device as a substrate for AI.

🤖 The WWDC Test and the M5 Squeeze

The Revamp of Siri? It has lagged behind every major competitor for years, dropping context, returning search results instead of answers, and failing basic multi-step requests. The WWDC 2026 keynote on June 8 is expected to center on a revamped Siri in iOS 27, with a new Dynamic Island interface, a standalone Siri app with conversation history, and multi-command support. Bloomberg's Mark Gurman reports the glowing "26" in Apple's WWDC invite is teasing the new Siri.

The Hardware Struggles: The M5 Pro and M5 Max launched in March on TSMC's 3nm process with AI tasks running 3.5x faster than M4. Yet the Mac Studio M5 Ultra may slip to October due to the global DRAM shortage. Configurations with 128GB and 256GB RAM are currently unavailable. Wait times have hit 12 weeks. The touch MacBook Pro is also expected to slip. Apple reported a record 30% recycled material across all 2025 products and 100% recycled cobalt in all batteries.

Translation: Cook grew Apple from $350B to $4T and is handing the keys to a hardware engineer in the middle of an AI credibility crisis. If the best hardware company in the world can't ship a competitive AI assistant or keep its pro hardware in stock, will the $4T valuation hold?

🧑💻 OpenAI's $852B Identity Crisis

📋 The Leaked Memo

OpenAI's $852B valuation is under scrutiny from its own investors. On April 13, CRO Denise Dresser sent an internal memo that leaked within 24 hours. The four-page document reveals a new model codenamed "Spud" and names three enterprise products: Frontier, DeployCo, and an expanded ChatGPT for Work bundled with Codex.

Anthropic in the Crosshairs: Dresser claims Anthropic inflates its revenue by ~$8B by grossing up revenue-share payments to Amazon and Google, bringing its real run rate closer to $22B than the reported $30B. Enterprise now accounts for 40% of OpenAI's total revenue and is on track to match the consumer business by year-end. Dresser noted that demand since the Amazon Bedrock partnership has been "frankly staggering," signaling friction with Microsoft's exclusivity.

🚪 The Departures and $852B Question

And three more senior leaders left. Kevin Weil (VP of OpenAI for Science) is out; Prism will be shuttered. Bill Peebles (Sora) and Srinivas Narayanan (CTO of enterprise apps) are also leaving. This follows three Stargate infrastructure leaders who left for Meta earlier this month.

Some shareholders are questioning whether Altman should lead OpenAI through an IPO and have floated Bret Taylor as a successor. One early backer: "You have ChatGPT, a 1 billion-user business growing 50-100% a year; what are you doing talking about enterprise and code?" OpenAI has revised its product roadmap twice in six months.

💰 The Anthropic War Chest and Cerebras Gambit

The Competitive Pressure: Amazon is investing another $25B in Anthropic, on top of the $8B already committed, making it the largest corporate AI investment in history. Anthropic will spend $100B+ on AWS infrastructure over 10 years. That dwarfs the Microsoft-OpenAI partnership in both capital and lock-in. If Dresser's leaked memo was meant to rally troops against Anthropic, the timing could not have been worse.

While talent leaves, OpenAI is locking in chips. OpenAI agreed to pay Cerebras $20B+ to use its server chips, double the previously reported amount. Cerebras filed to go public on Nasdaq with $510M in 2025 revenue (up 76% YoY) and a target valuation of $35B+.

On the consumer side, ChatGPT ad rates are falling from $60 CPM to as low as $25 CPM, and the minimum spend has dropped from $250K to $50K. OpenAI launched GPT-Rosalind for life sciences and GPT-5.4-Cyber for cybersecurity, both to limited partners. The pattern: vertical models for enterprise, while ad revenue disappoints.

Translation: OpenAI's CRO leaked a war plan against Anthropic, accused it of inflating revenue by $8B, and revealed a new model and three enterprise products. When your own CRO is writing internal attack memos about the competition while your rival just locked up $33B in backing and a decade of infrastructure, is the $852B valuation pricing in a turnaround or a company being outspent?

💻 The AI Coding Gold Rush

🚀 The Cursor Constellation + Dev Effects

The tools that build software are now worth more than most of the software they build. Cursor is in advanced talks to raise about $2B, co-led by a16z at a pre-money valuation of more than $50B, with Nvidia participating. At that price, Cursor would be worth more than Figma, Canva, and most of the design tool industry combined. Also, xAI plans to let Cursor train its Composer 2.5 AI coding model using tens of thousands of xAI's GPUs.

The Job Data: Software engineering roles grew by 67,000 in Q1, even as 80,000 other white-collar jobs were cut across the tech industry. And companies are buying Slack, Jira, and email archives from defunct startups to train AI agents in simulated workplaces. But the economics are already breaking.

The App Growth: App releases across the App Store and Google Play grew 60% YoY in Q1, with App Store releases alone up 80%. The likely driver is that AI coding tools are lowering the barrier to shipping.

⚠️ The Platform Crunch

The Economics of AI: Microsoft paused new signups for GitHub Copilot Pro, Pro+, and Student plans, tightened usage limits, and removed Opus from the Pro tier, limiting 4.7 to Pro+ subscribers. Internal docs show Copilot's per-user costs have nearly doubled since January. The most popular AI coding tool in the world is hitting a wall where usage growth outpaces revenue.

The Competition: Sergey Brin told DeepMind staffers to aggressively pivot resources toward coding agents, forming an internal strike team to catch up on the agent race. Also, Moonshot AI released Kimi K2.6, an open-weight model that is beating closed models on long-horizon coding benchmarks.

Translation: Yes, Cursor is worth $50B. But GitHub Copilot just paused signups because costs nearly doubled, Google formed a coding agent strike team, and an open-weight model from China is beating closed models. If the biggest AI coding platform can't make the economics work while three new competitors are racing to replace it, what does the market look like in 12 months?

🧠 The Global Memory Crisis

📱 The Consumer Squeeze

The Memory Compaction: The global DRAM supply will meet only 60% of demand through 2027, as chipmakers prioritize high-bandwidth memory for AI over commodity DRAM. Memory is expected to hit ~40% of low-end smartphone manufacturing costs by mid-2026, up from 20% now.

The Squeeze: Meta raised the Quest 3's price by $100 to $599.99, citing a memory shortage. Also, global smartphone shipments fell 4.1% YoY in Q1, the first drop since mid-2023. India fell 3% to a six-year low, with 80+ smartphone models seeing price hikes of ~15%.

🔬 The Chip Makers' Response

The companies making chips are thriving even as supply falls short. TSMC reported Q1 revenue up 35.1% YoY to ~$35B, net income up 58.3% YoY to ~$18B, both above estimates. Advanced chips (7nm or smaller) were ~74% of wafer revenue. CEO C.C. Wei said he checked with customers about AI demand amid the Iran war and was reassured it remained strong. TSMC raised revenue forecasts.

ASML reported Q1 net sales of €8.8B and raised its 2026 forecast to €36B-€40B. South Korea surpassed China as ASML's largest market in Q1, accounting for 45% of net system sales. Google is in talks with Marvell to develop a memory processing unit for TPUs. SK hynix began mass production of 192GB SOCAMM2 modules for Nvidia's Vera Rubin platform, further redirecting memory toward AI servers.

Translation: The AI boom is creating a two-tier chip economy: one that serves $50B coding startups and hyperscaler data centers, and one that serves everyone else. If you're building consumer hardware, how do you compete for memory against companies willing to pay any price for compute?

Diskless, Kafka-Compatible Streaming That Runs in Your Cloud

WarpStream BYOC is a diskless, stateless Kafka-compatible streaming platform. No local disks, no inter-AZ fees, no broker rebalancing. Your data stays in your own cloud. Agents auto-scale automatically.

Robinhood uses it for logging. Cursor runs AI telemetry on it. Grafana Labs streams at 7.5 GiB/s with zero cross-AZ fees. Change one URL, keep all your existing clients. Learn more, or sign up for free.

Get $400 in credits that never expire. No credit card required to start.

⚡ Startup Quick Hits

Recursive Superintelligence: $500M+ for the four-month-old startup developing self-teaching AI, founded by ex-DeepMind and OpenAI engineers

DeepSeek: $300M+ at $10B+ valuation, the Chinese lab's first outside funding round

Upscale AI: $180M-$200M at $2B for AI networking infrastructure; third funding round in seven months

Factory: Raised a $150M Series C led by Khosla at a $1.5B valuation; its AI coding agents switch between models depending on task complexity

Drift Protocol: $147.5M from Tether and partners to replace Circle stablecoin with USDT after a $270M exploit linked to North Korea

Slash: $100M led by Ribbit at $1.4B for the financial services AI agent; nearly $300M in annualized revenue

Loop: $95M Series C co-led by Valor for AI that predicts supply chain disruptions

Artemis: $70M Series A led by Felicis for the AI-driven cybersecurity platform replacing rule-based systems

Expo: $45M Series B led by Georgian for the React Native framework and cross-platform cloud services

Mintlify: $45M Series B at $500M led by a16z and Salesforce Ventures for AI-generated software documentation

CuspAI: $200M+ at $1B+ for AI-driven materials discovery; backed by Lux Capital

💰 Investor Quick Hits

Sequoia: Raised ~$7B for a new fund, the first under its new leadership; its last expansion fund was $3.4B in 2022

Iconiq: The wealth manager has $100B AUM with $26B for VC; invested $3B into AI startups in 2025

Jane Street: Took an additional $1B CoreWeave stake and plans to spend ~$6B to access Nvidia Vera Rubin chips

SoftBank: Inviting more banks to join its $40B loan backing its OpenAI investment; each must commit ~$5B

US late-stage VC: Growth and late-stage funds raised $23.6B YTD, above totals for any of the past 12 years, driven by AI

European VC: Q1 funding rose nearly 30% YoY to $17.6B; AI claimed 50%+ of all European funding; deal volume fell 40%

💸 IPO & M&A Quick Hits

Netflix Q1: Revenue up 16% YoY to $12.25B, net income up 83% to $5.28B; Reed Hastings stepping down from board in June; Q2 forecast below est., NFLX drops 10%+

Kraken/Bitnomial: Payward acquires the digital asset derivatives platform for up to $550M in cash and stock, valuing Payward at $20B

OnlyFans: In advanced talks to sell a below-20% stake at a $3B+ valuation, down from earlier reports of a ~60% stake at ~$5.5B

Manycore: Hangzhou-based company rose 187% in its Hong Kong debut after raising $156M; pivoting to selling AI training data for robots

Google/SpaceX: Google owns a ~5% SpaceX stake; if SpaceX hits a $2T IPO valuation, Google's position would be worth $100B

eToro/Zengo: eToro acquires crypto wallet provider Zengo for ~$70M, mostly cash; Zengo enables swaps between tokens and fiat

🌟 Editor's Note

At Startup Intros, our mission is to bring the latest founder-investor news straight to your inbox, keeping you ahead in the fast-paced world of Silicon Valley.

💭 Parting Thoughts

Tim Cook stepped down after growing Apple from $350B to $4T. His successor built Apple Silicon and Vision Pro. Amazon committed $33B to Anthropic. OpenAI's CRO leaked a war memo the same week three more leaders walked out. GitHub Copilot paused signups because costs nearly doubled. Cursor hit $50B. Google formed a coding agent strike team. DRAM will run at 60% supply for two years. App releases jumped 60%. Meta is cutting 8,000. A four-month-old startup raised $500M.

The weeks keep showing how AI has become a platform war. Apple is betting on hardware in the middle of an AI credibility crisis. Amazon is betting $33B that Anthropic wins the enterprise. OpenAI is writing attack memos about it. Microsoft's Copilot economics are breaking. Google is scrambling to catch up on agents.

Every major platform is repositioning at the same time. The capital has never been larger, and the uncertainty has never been higher.

Till next time!

| Dev Chandra |

Startup Intros Weekly Download: Your trusted source for founder-investor insights, delivered with clarity and focus.